“You are free in inverse proportion to the number of people to whom you can’t say ‘fuck you.’ But you are honorable in proportion to the number of people to whom you can say ‘fuck you’ with impunity but don’t.” —Nassim Taleb

The parable about the fisherman and the businessman is beautiful, but dangerous.

If you haven’t heard it before, it goes something like this:

A fisherman in a small coastal village catches just enough fish each day to support his family and spends the rest of his time enjoying life—spending time with loved ones, playing music, and relaxing on the beach. One day, a businessman visits the village and suggests the fisherman could work harder, catch more fish, and reinvest his earnings to grow a fishing empire. He explains that with time, the fisherman could hire others to do the fishing, allowing him to retire rich and finally relax. To which the fisherman responds, “But isn’t that what I’m already doing?”

The parable brilliantly illustrates the concept of “enoughness.” But like many utopian visions, it fails to account for the inherent unpredictabilities of real life.

What if the fisherman’s country faces political unrest or war? Wealthy Jews, for example, found it easier to escape Nazi Germany than their poorer counterparts.

Or what if a drought, pollution, or overfishing depletes the fish population? Or a storm wipes out his boat?

What happens when the fisherman gets older and his physical ability to fish declines?

And how has this idyllic fishing village escaped the omniscient gaze of both BlackRock and Hilton, and with them scores of tourists and more technologically-advanced industry, including fishing?

Add in the fact that most of us don’t live in a detached fishing village, or even know how to fish, and you can start to see the dangers of following the philosophy of the fisherman.

A (Highly-Solvable) Crisis

Like the fisherman completely at the mercy of external forces, nearly 60% of Americans are living paycheck to paycheck.1

What would happen if you lost your job or faced an unexpected medical bill? Crippling debt? Bankruptcy? Homelessness?

Financial illiteracy is a legitimate crisis.

But there is good news. While the businessman suggested the fisherman work harder to achieve independence, I suggest you can achieve independence while doing less work, at least when it comes to managing (or worrying) about your finances.

And the best part? With independence you unlock a whole new world of opportunity. You could live according to your values and goals and chosen pursuits. You could stop trading your today’s for future tomorrow’s.

You could say “F-You” to anyone who asks you to compromise your values—but choose not to. The alternative is terrifying. The stakes are literally life-changing.

But how do we get there?

For answers, let’s turn to a janitor from Dummerston, Vermont.

The $8 Million Janitor and Three Simple Rules

“Ronald Read was an American philanthropist, investor, janitor, and gas station attendant.”

What do you notice about the first sentence of Ronald Read’s Wikipedia page?

That you’ve never seen “philanthropist” associated with “janitor?” Or maybe you’re wondering how a man with such modest jobs even has a Wikipedia page. Or are you still stuck on the section header trying to figure out how a janitor died with a net worth of $8 million?

I’ll skip to the punchline—he followed the three simple rules2 to accumulate wealth:

Avoid debt.

Spend less than you earn.

Invest the rest.

Steps one and two are self-explanatory and difficult largely thanks to human nature and a coordinated effort to get you to spend more.

Fear and misconceptions around step three is a common roadblock for many people, so we’ll cover the “how” and “how much” below.

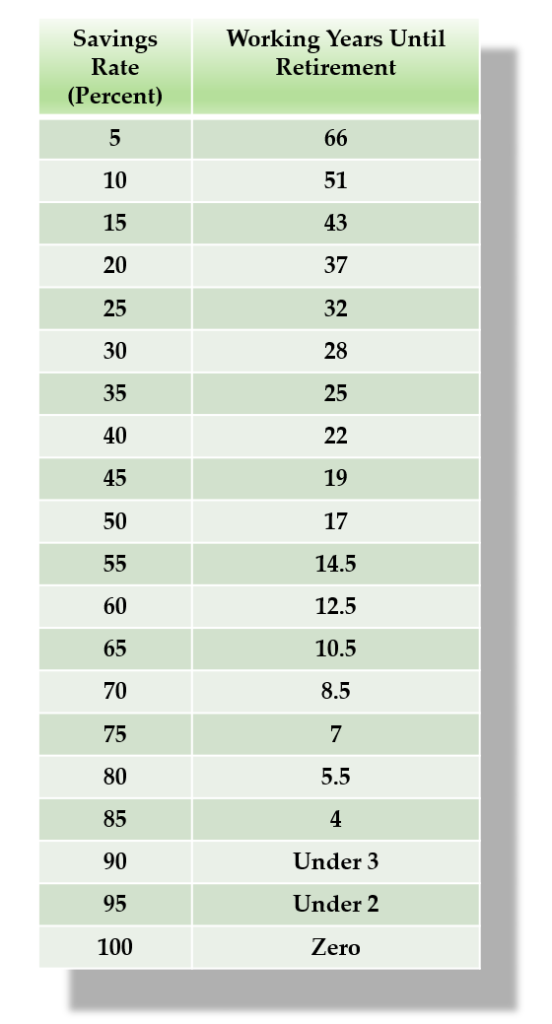

But first, let’s talk about the little-known most important factor in your time to independence: savings rate.

The Single Biggest Win: Savings Rate

How could someone like Ronald Read, who likely earned around $30,000 per year, die with almost $10 million, while Mike Tyson, who earned $30,000,000 per fight, end up bankrupt?

The answer is not-so-shockingly simple: he spent less relative to his income.

Lest I lose your interest, this isn’t a call to a spartan lifestyle. (Ronald might have found more balance, and Iron Mike definitely could have used more impulse control.) Rather, it’s to highlight the immense impact small changes to your savings habits can have on your journey to independence.

For instance, an average earner bringing home $50,000 annually and saving 5% could shave 15 years off their time to retirement by simply saving an additional $48 per week. That’s one round of drinks on the weekend!

Credit: Mr. Money Mustache. For further reading, see here.

Let me repeat, the goal is not asceticism.

The goal is awareness—understanding the trade-offs in your financial decisions so you can make the best choice for yourself. Too many people overlook the opportunity costs of their decisions, ranging from that round of drinks to buying a home.

While the debate between “earning more” vs. “spending less” rages on in the personal finance world, one thing is certain from our opening example: it doesn’t matter how much you earn if you’re not saving a portion of it.

And remember, your savings rate is a flexible lever. You can increase it by boosting your income or by cutting expenses—or ideally, a bit of both.

That’s why focusing on increasing your savings rate is the single biggest win in your path to financial independence.

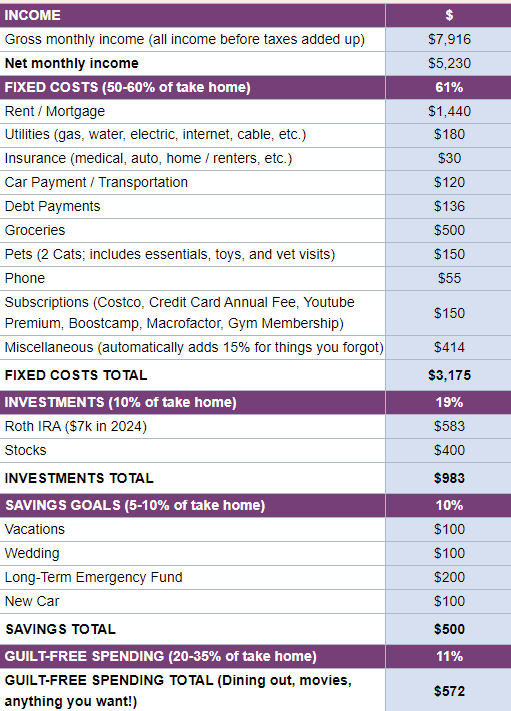

Plan with Buckets, not a Budget

So, how does this look in practice?

Let’s go step-by-step:

Set a realistic target savings rate.

List your expenses from the past three months.

Categorize each transaction (e.g., “401k transfer,” “dining,” “rent”).

Group these transactions into four major buckets: “Fixed costs,” “Investments,” “Savings goals,” and “Guilt-free spending.”

For each month, calculate your actual savings rate. (Add your savings and investments, divide by take-home pay, then multiply by 100.)

Compare your actual savings rate to your target. If your rate exceeds your goal, celebrate! If it falls short, still celebrate—then look for ways to close the gap.

Here are Ramit Sethi’s suggested target allocations for reference:

Fixed costs (rent, utilities, debt, etc.): 50-60% of take-home pay

Investments (401k, Roth IRA, etc.): 10%

Savings goals (vacations, gifts, house down payment, emergency fund, etc.): 5-10%

And here’s an example of what this breakdown could look like:

Courtesy of iwillteachyoutoberich.com

These recommendations offer a great starting point. But if your goal is financial independence, remember: achieving uncommon goals requires taking uncommon actions. According to the savings rate chart in the previous section, Ramit’s recommended 15-20% savings rate could still mean working for another 37 to 43 years.

Personally, I’d prefer to bring that number much lower.

But the most important step is simply getting started—even if it’s just $50.

In the next section, we’ll tackle the basics of investing and show how even a small amount can grow significantly through the power of compounding.

The 80/20 of Investing

“But the most important step is simply getting started—even if it’s just $50.”

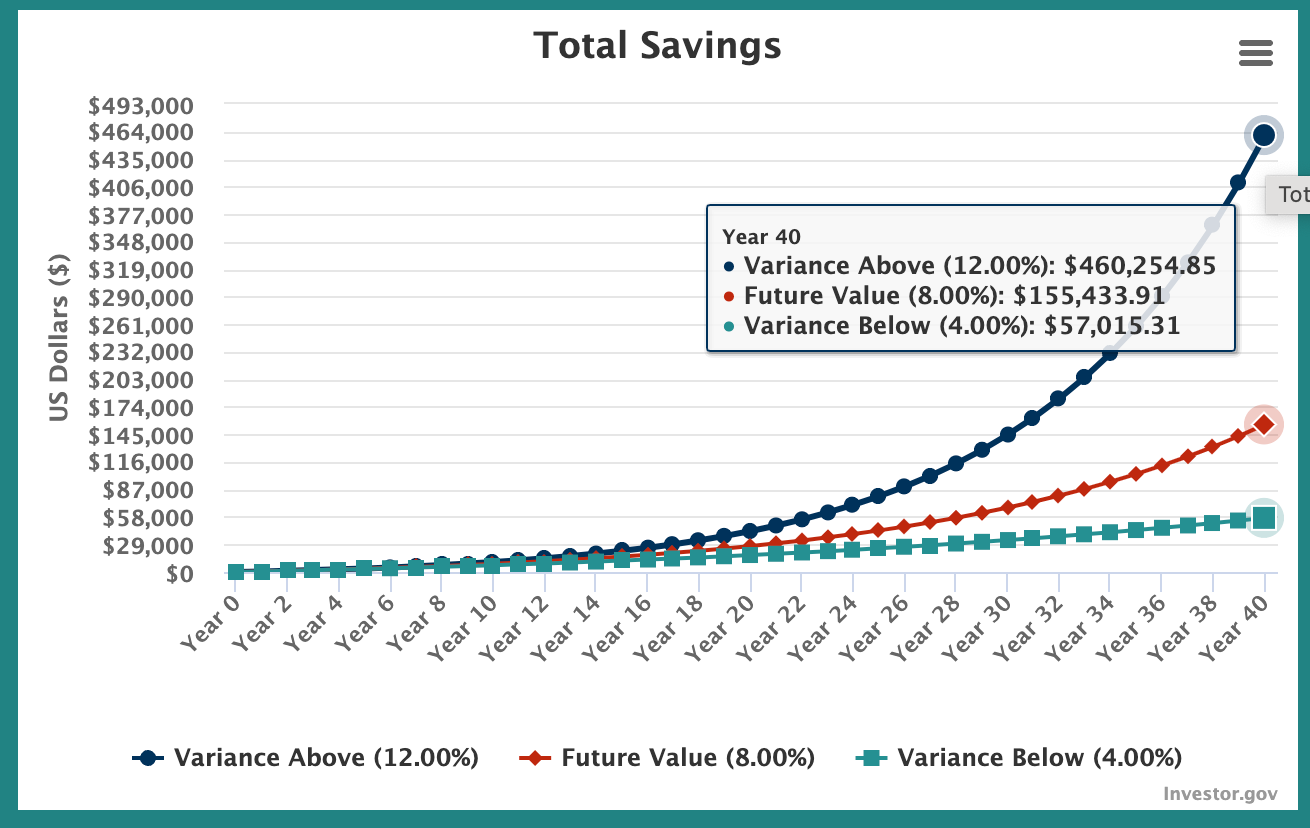

This wasn’t a throwaway comment. Let’s see what happens when you invest $50—an amount you’d hardly notice was gone—each month for 40 years, thanks to the magic of compound interest.

Your initial $24,000 investment ($50/month x 40 years) could become a not-so-insignificant:

$57,015 at 4% (similar to a high-yield savings account)

$155,434 at 8% (a conservative estimate of market returns, given historical averages of 8% to 10% with dividends reinvested)

$460,255 at 12% (roughly the average S&P 500 return over the past 40 years)

Let’s consider a few more scenarios to fire up the imagination.

Take the same $50,0003 earner from earlier. If they diligently invest 5% of their income, or $208 per month, they could accumulate $237k, $647k, or $1.9 million,4 depending on the same 4%, 8%, and 12% rates.

If they invest 10%, or $417 per month, their savings could jump to $476k, $1.3M, or $3.8M, using the same rates.

If you’re like me, a few things stand out: the huge difference between 4% and 12% returns, the exponential growth of even a small starting amount, and the relatively flat growth in the first 20 years followed by a rapid ascent.

We’ll break down each of these points briefly.

$470 Thousand or $3.8 Million

For our average earner investing 10% of her $50,000 income, that’s the difference between putting her money into a high-yield savings account versus the S&P 500’s 40-year returns.5

More importantly, it’s the difference between waking up to an alarm every morning and starting each day with the freedom of a blank canvas.

Can you start to see why investing, even in small amounts, is imperative compared to simply saving?

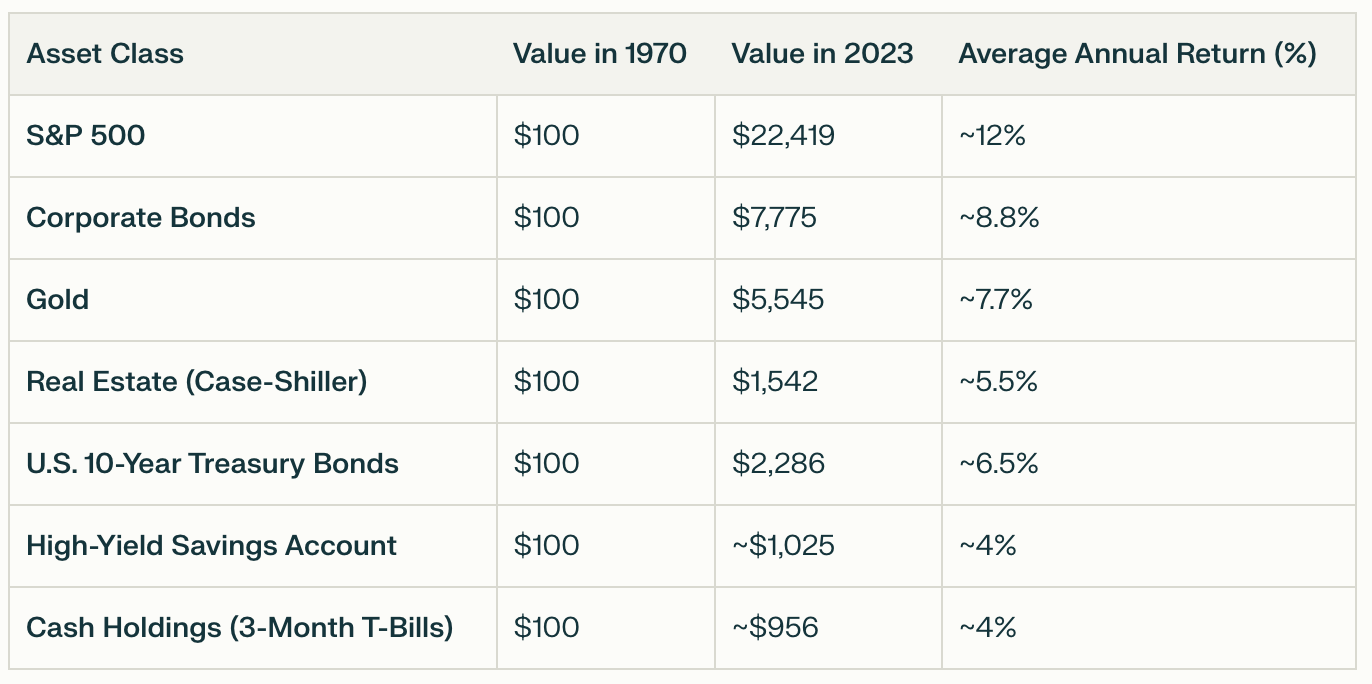

This is the right moment to mention that I won’t ever recommend any single investment vehicle over another (see the section below: “Advice: Don’t Listen to Investment Advice”). However, because no other asset classes have outpaced the stock market over the long term, I use it as a benchmark. Add in the fact that it’s a passive investment requiring little to no management, comes with low fees (expense ratios), and is accessible to nearly anyone, it’s currently the gold standard for most people. But that doesn’t mean it will always be. No one can predict the future. So whether you’re investing in yourself, starting a business, buying real estate or Pokémon cards, the same principles apply: avoid debt, spend less than you earn, invest the rest.

Armed with historical data, sound logic, and a clear sense of what not to do (covered below), you can make a decision about what’s the best investment for you.

Personally, I currently invest in three main areas: myself (through skill development), the US stock market (VTSAX), and a combination of BTC/ETH/SOL. While not everyone would agree with this approach, I have my reasons, and I sleep well at night.

A common rebuttal is that investing is "risky." Let’s address that. According to the Cambridge Dictionary, risk is "the possibility of something bad happening."

If we accept this definition, then risk is unavoidable.

Every decision and action carries some level of risk, so instead of trying to avoid it altogether—which is impossible—we should focus on calculating and managing it effectively.

For me, the risks of not investing—such as losing purchasing power to inflation and missing out on growth opportunities—far outweigh the risks of investing.

As with most things, it’s important to learn the rules so you can break them effectively.

However, some rules are better left unbroken. We’ll cover those next.

Compound Interest’s Evil Twin

As mentioned earlier, one of the biggest risks of not investing is the lost potential for long-term growth, also known as “opportunity cost.”

Think of opportunity cost as the evil twin of compound interest.

It’s the inspiration behind all those “skip your latte, become a millionaire” clickbait articles.

Though the “skip a latte” argument is flawed (where does it stop?), the premise is sound: small amounts of money grow exponentially over time thanks to compound interest. Spend that money elsewhere, and you miss out on the interest it would have earned—along with the compounding interest on that interest.

It’s worth repeating: this isn’t about asceticism; it’s about awareness.

Once you understand the trade-offs, you might decide your daily coffee is worth the cost—and that’s great. But what about bigger purchases, like a car?

Take, for example, choosing between a $20,000 car and a $30,000 car. The $30,000 option isn’t just $10,000 more—it’s $10,000 plus the interest that money could have earned, and the compounding interest on top of that interest, ad infinitum.

The effect is even more pronounced if you finance the car. Now, you’re not only missing out on compound interest—you’re actually paying interest on the loan.

Remember the earlier chart showing how $100 grew over time? And how saving $48 per week impacted your retirement forecast to the tune of 15 years? I’ll let you do the math on the car purchase.

I know I’m sounding like a broken record, but here’s one more example to show how a long time horizon can make seemingly trivial amounts grow significantly. We’ll compare using a commission-based financial advisor with investing in the S&P 500, using the 10% saver example from earlier.

Scenario 1 (No financial advisor fee):

$0 initial investment

$5,000 annual contributions ($417 per month)

8% return over 40 years

Final value: $1,295,283

Scenario 2 (With 1% advisor fee):

$0 initial investment

$5,000 annual contributions

7% return over 40 years

Final value: $998,176

In Scenario 1, your money grows at 8% over 40 years, resulting in about $1.3 million. In Scenario 2, the 1% advisor fee reduces your return to 7%, costing you nearly $300,000 over the same period.

But wait, there’s more! The S&P 500 is also appealing because of its extremely low expense ratios. For example, the Vanguard VOO fund has an expense ratio of just 0.03%, compared to the 0.42% average6 for actively managed mutual funds with an advisor.

After factoring in expense ratios, here’s how the numbers break down:

Scenario 1 (0.03% expense ratio): With a 0.03% expense ratio, $5,000 annual contributions, and an 8% market return over 40 years, your investment would grow to $1,285,097.

Scenario 2 (1% advisor fee + 0.42% expense ratio): With a 1% advisor fee and a 0.42% expense ratio, your effective return drops to 6.58%, and after 40 years, your final amount would be 896,251.

The difference is eye-popping: Scenario 2 leaves you with $388,846 less than Scenario 1 due to the combined impact of the advisor fee and higher expense ratio.

And this assumes equal returns. In fact, the S&P 500 outperformed most actively managed large cap stock funds for the 14th year in a row.7 Approximately 88% of actively managed large-cap funds underperformed the S&P 500 over the long term.8

To summarize, an average earner investing a modest amount could pay nearly $400,000 in fees to a commission-based advisor over 40 years, only to almost certainly underperform the market.

The madness!

By now, it should be clear: you want to keep your money in the market and avoid unnecessary fees.

But what about the classic advice to “buy low, sell high”?

Time in the Market > Timing the Market

“The big money is not in the buying or selling, but in the waiting.” —Charlie Munger

Advice: Don’t Follow Investment Advice

Behind every investment strategy, there’s at least one charismatic evangelist with a persuasive pitch.

My advice: never blindly follow investment advice from anyone. This includes the obvious culprits whose follies range from misaligned incentives to downright deceit: financial influencers, media pundits, and the most dubious of all, commission-based financial advisors.

If they could consistently beat the market, do you think they’d be spending their time sharing those strategies with you out of the pureness of their soul?

But this advice extends even to well-intentioned family and friends—and yes, even me.9

Even if they’re financially savvy (a big “if”), their circumstances, values, and goals will likely differ from yours—at least to some extent.

So how can an inquiring novice cut through all the noise? There are two ways:

Study historical trends and undeniable math (like the S&P 500’s long-term returns vs alternative assets and the power of compound interest).

Learn what not to do.

Just as happiness often comes from eliminating unhappiness, financial literacy often stems from understanding financial mistakes—or simply knowing what not to do.

And now you’re aware of some of the biggest no-no’s that will keep you shackled to financial struggles:

Ignoring the three fundamental rules: avoiding debt, living below your means, and consistently investing.

Failing to understand the opportunity costs of your financial decisions.

Attempting to time the market.

By understanding the most rational financial choice in any situation, you’ll be able to confidently make reasonable decisions tailored to your unique circumstances.

YNAS: You Need a System

At this point, you might be wondering, “If it’s so simple, why isn’t everyone a millionaire?”

My response, though annoying, would be: “Well, it’s simple, but not easy.”

Why? Because humans are naturally wired to prioritize immediate gratification over long-term benefits—a tendency known as poor time preference.

This behavior is deeply embedded in our evolutionary makeup. When food was scarce, it made sense to consume as many calories as possible. Without a way to multiply resources for the future, people would naturally spend what they had.

And evolution, as we know, is a slow process.

One of the first stock exchanges, The Amsterdam Stock Exchange, opened in 1602—about 301,602 years after the emergence of the first humans.

In another 300,000 years, we’ll likely be better tuned to investing.

In the meantime, we’re battling not just our own human nature, but also cultural conditioning and a consumer-driven society—amplified by a billion-dollar advertising industry that has nearly perfected psychological manipulation.

Put together, it’s far from easy.

Thinking about personal finance usually engages system two, the brain's more energy-intensive mode of thinking. We must remain aware of our habits, track spending, resist impulses, and plan to optimize our income, which can be mentally exhausting.

So instead we buy the latest gadget, hire a personal driver for our takeout, complain about delivery fees owed to said driver, criticize the previous generation for not understanding our struggles, and binge-watch Netflix.

And so the dreadful personal finance cycle continues—guessing, hoping, checking, scolding, regretting, repenting, and repeating.

We need a system that protects us from us.

I’m working on building that system. But for now, manually setting up this system to automate your finances is a great place to start.

Your Life and Civilization Are at Stake

“Civilization is not about more capital accumulation per se; rather it is about what capital accumulation allows humans to achieve, the flourishing and freedom to seek higher meaning in life when their base needs are met.” —Saifedean Ammous

Now that you have a recipe, a day will come—presumably sooner than anticipated—when you’ll no longer have to trade today for tomorrow.

And you alone will decide how to seize that day.

Will you travel the world, marveling at its divine beauty? Will you finally dedicate time to mastering that elusive skill you’ve always longed to learn? Or will you pour your energy into a passion project, making your corner of the universe a better place to inhabit?

Life will be yours to bathe in.

The personal benefits are obvious. The desire for freedom—whether from shackles or neckties—has existed since the dawn of mankind.

"...because all man's efforts, all his impulses to life, are only efforts to increase freedom. Wealth and poverty, fame and obscurity, power and subordination, strength and weakness, health and disease, culture and ignorance, work and leisure, repletion and hunger, virtue and vice, are only greater or lesser degrees of freedom." —Leo Tolstoy

But can the accumulation of individual wealth benefit society and help advance civilization?

Despite cultural conditioning that fosters a near-sociopathic disdain for wealth and its holders, the answer is a resounding “yes.”

Could da Vinci have painted the Mona Lisa after a long day laboring on the farm? Would Newton have seen that apple fall and discover gravity while staring out the window of his cubicle? Could Darwin, as a factory worker, have formulated the theory of evolution?

John Adams famously said, "I must study politics and war that my sons may have liberty to study mathematics and philosophy. My sons ought to study mathematics and philosophy, geography, natural history, naval architecture, navigation, commerce, and agriculture, in order to give their children a right to study painting, poetry, music, architecture, statuary, tapestry, and porcelain."

In that same spirit, we must accumulate and pass down wealth so that our children have the freedom to learn and create amongst the stars.10

Any time I mention the “S&P 500’s 40-year returns,” I am referring to the period between 1975 and 2015. I was unable to find data for the most recent 40-year period (1983–2023). Although significant fluctuations in the average over time are unlikely, even small percentage changes across a 40-year span can have a large impact on returns. If you have data on the most recent 40-year period, I’d love to hear from you!

While investing in low-cost index funds tracking the S&P 500 has proven to be an effective strategy for many, it’s important to consider individual circumstances: risk tolerance, time horizon, and overall financial goals. For some, a diversified portfolio with a mix of domestic and international stocks, bonds (lol), and alternative assets may be more appropriate. Remember, past performance does not guarantee future results.

This article is intended for informational purposes. The advice presented here is not entirely original, as it draws heavily on insights from various experts. The inspiration for this article came from running family finance workshops and a desire to consolidate the entire curriculum into one document. Much of the financial advice is based on the teachings of Charlie Munger, Morgan Housel, JL Collins, Ramit Sethi, Vicki Robin, and Peter Adeney.

The four books that have most influenced my views on personal finance are The Simple Path to Wealth by JL Collins, Your Money or Your Life by Vicki Robin, I Will Teach You to Be Rich by Ramit Sethi, and The Psychology of Money by Morgan Housel. I have read and revisited these books multiple times, to the point where the lines between their ideas and my own have blurred. I’ve attempted to give credit where due—for example, to Collins for his three rules, Sethi for his categorization and system, and Adeney for his insights on savings rate. However, there may be other instances where proper attribution is warranted.

If you find a good idea in this article, it likely originates from one of these great thinkers. If you find a bad idea, the responsibility is mine alone.

Sam, really great post! You seem to have a knack for breaking down complex topics and explain them in a super accessible way. And as much as I identify with the Mexican fisherman (no surprise there, huh?), this was a great kick in the butt to take another look (🫣) at my finances. Excited to read more of your writing going forwards!

Sam, really great post! You seem to have a knack for breaking down complex topics and explain them in a super accessible way. And as much as I identify with the Mexican fisherman (no surprise there, huh?), this was a great kick in the butt to take another look (🫣) at my finances. Excited to read more of your writing going forwards!